The national rental index increased by 0.6% in July, the 35th consecutive month of increases, but the smallest month-on-month rise since December 2021.

Slowing rental growth has been most evident across regional areas of Australia, where the combined regionals rental index increased by only 0.2% in July, the lowest monthly rise in regional rents since June 2020. Alongside the easing in rental growth, regional vacancy rates have moved higher, from a low of 1.3% in early 2022 to 1.6% in July. Although regional vacancy rates have risen, they remain half of the decade average (3.2%).

Capital city rental growth has also slowed, recorded at 0.8% in July, which was the lowest monthly rise since December last year. Hobart (-2.1%) and Canberra (-1.1%) were the only capitals to record a drop in rents over the most recent three-month period. These are also the only two capital cities where vacancy rates have risen more than a percentage point over the past 12 months, reflecting a better balance between rental supply and demand.

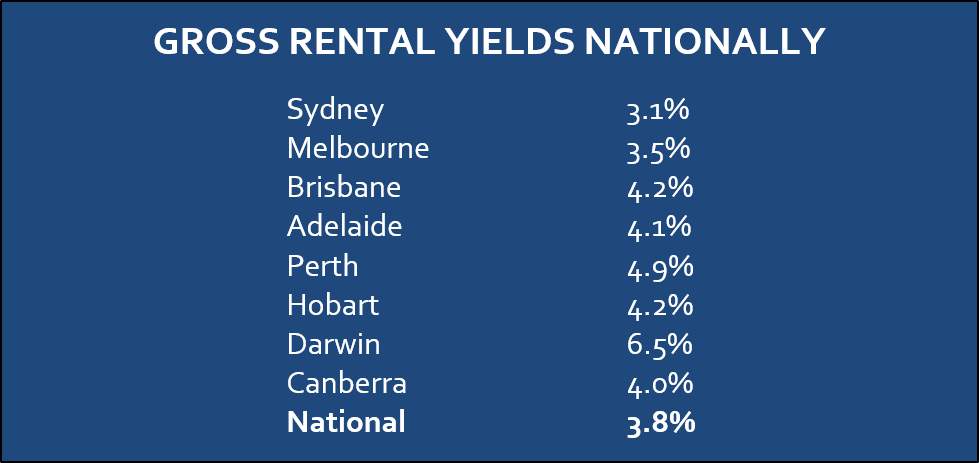

The strongest rental conditions continue to be seen across the unit sector, where rents were up 2.9% over the three months to July nationally, compared with a 1.9% rise in house rents. Looking at the data in more detail, across the capital city and rest-of-state regions, the unit markets of Perth (4.3%), Melbourne (4.0%) and Brisbane (3.8%) stand out with the fastest rate of rental growth over the rolling quarter.

At the other end of the spectrum, the largest decline in rents over the rolling quarter was in Regional NT, where house rents were down – 6.4% over the past three months, alongside Hobart where house rents were down -2.2% and unit rents were -2.0% lower.

Since January 2022, the unit sector across the capital cities has consistently shown a higher rate of appreciation compared to houses. This is likely due to several factors such as more affordable unit rents, increased demand for medium to high density accommodation, and supply constraints with approvals below the decade average since 2018.

Housing value growth moderates as listings rise

CoreLogic’s national Home Value Index (HVI) rose 0.7% in July, marking a fifth consecutive month of housing value recovery. Since finding a floor in February, the national HVI is up 4.1%, following a -9.1% decline from record highs in April 2022.

Nationally, home values remain -5.3% below the April 2022 peak, with only Perth, Adelaide and Regional South Australia recording a new cyclical high in dwelling values through July.

While housing values are continuing to record a broad-based rise, the rate of growth has marginally lost momentum over the past two months, slowing from 1.2% in May.

CoreLogic Research Director, Tim Lawless, says the most substantial reduction in growth has occurred in Sydney.

“After leading the upswing, the monthly pace of growth in Sydney housing values has halved from a recent high of 1.8% in May to 0.9% in July. Sydney has also seen a significant rise in the number of fresh listings added to the market, 9.9% higher than the same time last year and 18.0% above the previous five-year average. An increased flow of new listings provides more choice and may be working to reduce some of the urgency felt among prospective buyers,” he said.